Saudi Arabia’s Future Energy Mix: 40% Renewables, 35% Gas and 20% Oil

In 2014 we tendered many projects. Our record is, we submitted 11 tenders between 2013 and 2014, losing only 1 bid. So we enter 2015 with 10 new projects on hand.

Interview with Paddy Padmanathan, President and CEO of ACWA Power

What are the strategic objectives for ACWA Power, for the year 2015-16?

For us 2015 and 2016 are going to be very busy years. We are a startup, but now we are into our 11th year. Like many startups we have grown on a “s” curve growth model. We are now in the acceleration phase. We are doing more, we are operating in a much wider geographical area. We have operations in a dozen countries. Consequently, we are doing a lot more today.

In 2014 we tendered many projects. Our record is, we submitted 11 tenders between 2013 and 2014, losing only 1 bid. So we enter 2015 with 10 new projects on hand. We are in various stages of finalizing power purchase contracts, some are finalized and we are getting into construction, some are in the financing stage. All this activity will happen in 2015. As we near the end of 2015, we expect to see nearly a dozen projects in construction. It’s an all-time high for us. We’ve never had more than 4 projects in parallel construction before. We also have a backlog of tenders in preparation, which will be submitted in 2015. These will become works in progress in 2016. So we are moving into a very busy period.

These are the new projects. We already have the existing assets that are operational, they are well embedded and we continue to work on improving them, optimizing them and keep them performing. It’s business as usual but at a much faster pace, with a bigger footprint and across a more diverse fuel-mix platform. For example, we are bidding on one of the biggest wind power projects the world has ever seen, an 850 megawatt single tender in Morocco. We are doing more CSPs (Concentrated Solar Power) and very large photovoltaics, in addition to gas-powered power plants. We are also tendering for some coal-fired power plants. We are also getting into waste-to-heat– to-electricity. It’s an exciting period.

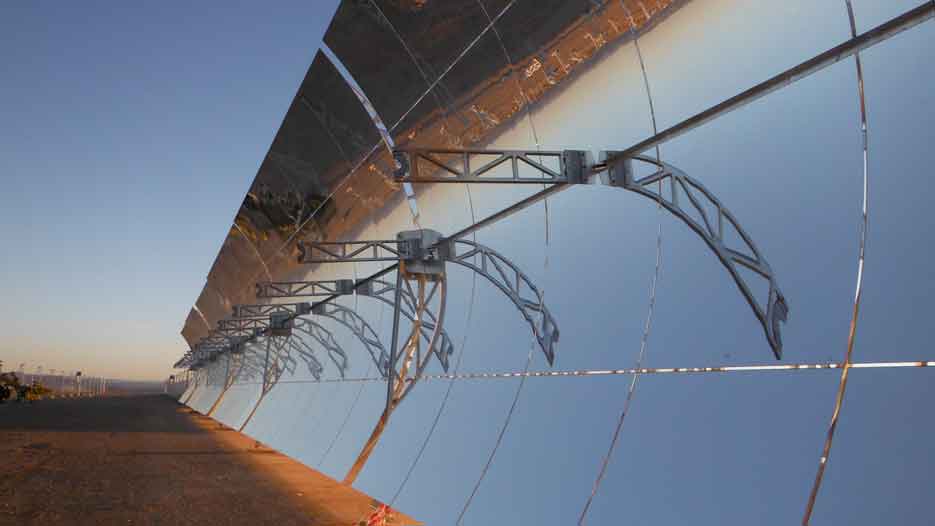

One of the interesting developments is that you recently tendered for a solar power plant in Dubai. You promised you would provide some of the cheapest electricity available. You came under a lot of criticism for that. A lot of people are skeptical that you can make any profit on this project. Can you talk about this a little?

Let me put it this way, we are not a charitable organization, we are a for-profit business. Only profit motivation can sustain activity over a long period of time. All I can say for sure is this, our tariff, the 5.845 cents per KW, which is about 20% lower than anything the world has seen before, is indeed stunningly low. I can well understand the skepticism. However, the fact of the matter is, it is achievable. We will achieve it and make a profit that is commensurate with the risks.

As this project has attracted so much attention, we have taken the unusual step of providing a much more detailed explanation than usual, as to how we were able to achieve this tariff. A high level breakdown would look like this. Probably half of the tariff will go towards the capital cost of constructing the plant. That includes the construction itself and the technology. About 30 to 35% will go towards the cost of getting it funded, financed. That includes both the debt funding and the equity, the profit that the equity investor makes. The balance, about 15%, is operational cost and maintenance. There is no fuel cost obviously, the good Lord has not figured out how to charge us for that.

We can look at each component. The easiest, and most impressive, one to look at is the 35% cost of funding. It’s very high. That’s because it is capital intensive. Renewable energy is capital intensive but operational expenses are low, because there is no fuel cost. We have to put together a lot of money up front. We borrow the money, we invest and we collect it back over 20 to 25 years. In this project, with the good credit of DEWA (Dubai Electricity and Water Authority), our off-taker, the well-established policy framework and the stability that Dubai provides, and presumably because of our own delivery track record, we were able to fund 86% of our project cost with debt funding. Typically in such projects, you might see about 80% funding by debt.

The higher the debt, the lower the cost because debt is cheaper. It’s cheaper because there is less risk for them than for equity investment. In this project, we don’t have the conventional 20% equity, we have just 14% equity. Even the debt that we got has a 27 year tenure. That’s unheard of. It’s based on a 25 year power purchase agreement. So we even have a tail on the debt. We were able to contract a long tenure debt and at less than 4% interest in total, it was a very competitively priced debt. Even the equity price is commensurate to the risks. It is not what people were expecting. Many people thought we wouldn’t be able to price it beyond single digit or make any money. We have priced equity at double digits, it’s over 10%. That package of 35% was very tightly optimized.

On the capital expenditure side of the project, contrary to what people think about photovoltaic plants, the panels are less than half the capital cost of the plant. It’s closer to 40% of the cost. We’re using First Solar panels. First Solar is the largest photovoltaic firm in the world. They are the industry leaders in efficiency, so the panels are very efficient which is very helpful. We have a very competent EPC contractor, TSK of Spain. About half the cost of the project is the construction of the plant. Dubai offers a fantastic construction platform. There’s a lot of construction capability and industrialization capability there. We are able to procure the balance of plant much more competitively. We don’t have to import a whole lot. The local content in this project is very high. So the capital expenditure, the 50% component, is also highly optimized.

The last 15% percent or so, is the operation and maintenance cost. As a matter of fact, we have nearly 2,000 people operating and maintaining our plants. We have 27 plants, though most of them are fossil fuel based. However, it gives us significant access to the supply chain, significant purchasing power and the ability to optimize across the platform, even in human resource capabilities. So we deliver O & M (operations and maintenance) competitively also.

All these strands drawn together bring us to this tariff. I am convinced that if DEWA were to offer tenders for another, similar plant, I would see an even lower tariff. This tariff would be the benchmark. There will be competition and the resulting tariff will be even better. It’s not a one-off marketing stunt. I’m often asked if these figures can be replicated in projects anywhere else in the world. No, you cannot, because credit conditions are different, sun intensity is different, number of daylight hours are different, ground conditions are different. Many variables influence the tariff. By 2014, photovoltaic energy costs had come down, but it was still about 13, 14 cents. Now, anywhere in the world, as long as there is enough sunlight, photovoltaic energy costs are in the single digits. It’s become very cost competitive, compared to any other form of energy in that segment of the demand curve.

Regarding your IPO, it’s caused a lot of buzz. You will be publicly listed soon. What can you tell us about it?

From the start, 11 years ago when we set up, we realized that water and power were the basic needs of economic development, sustenance of social stability and of life itself. Given the basic nature of these commodities I think it’s inconceivable that it should be entirely in private hands. Over time, the public have to be shareholders in it. But first the company needs to reach a position where the risks have been minimized and it has the ability to make profits on a steady basis and pay dividends.

No investor wants to put money into a company and then wait for 5 years as it builds assets, to realize some profit on investment. We needed to take our time building a portfolio of assets and establish a platform that could generate a steady dividend yield, which we can then start to share. It’s been a journey. We were founded by 3 private shareholders. Then another 5 more private shareholders came on board. Then we added a couple of institutional shareholders, Saudi Sovereign entities. Then we brought in the international finance corporation. The next logical step for us is to open our shareholding to the public. We are a Saudi company, so we will list in Saudi Arabia first. We have been working on it in 2014, and early 2015.

As for launch dates and the other details around it, it is all subject to regulatory approvals. We’ve come to a point where we cannot discuss it much more until we have all the regulatory approvals in place. Only then can we formalize the launch process and within the bounds of regulations we can say more about it publicly. What I can confirm is that we are absolutely committed to broadening the shareholder base to include the public. So there will be an IPO but it’s subject to regulatory approval, and the timeframe is based on that. We are preparing for it.

You have begun to bid on solar projects all around the world and win some tenders. Is this a major shift in your strategy or a continuation of your strategy? We have seen a significant downturn in coal prices, and coal is making a comeback. How do you see your future solar projects and their viability vis-à-vis the price of coal?

Good question and it gives me a chance to restate our business objectives. We were founded as a business that provides reliable electricity and desalinated water at the lowest possible price. We take a meaningful equity interest in the assets used in providing these services and operate and maintain plants. But, we are technology neutral and fuel agnostic. It’s not my business to tell my customer what to do. We respond to the customer’s preferences, the customer’s fuel choices and technology preferences. As we invest significant sums of money on our assets in all the countries where we operate, in Saudi Arabia, Vietnam or South Africa or wherever, we are concerned that those countries develop in a stable, sustainable manner.

We are very keen to ensure that they deploy the right resources for something as fundamental as power generation. We thus advocate and lobby, and try to show them that diversifying the fuel mix where they have alternative resources like the sun and the wind is cost competitive and how to increase their use. But other than that we respond to the customer’s requirements.

What we have seen, particularly in the last 3 to 4 years, is a very rapid shift. This is backed by more reliable data from agencies like the International Energy Agency. Renewables are being used preferentially over fossil fuel based energy. There are 2 very good reasons for this. First, and most obvious, is that renewable energy costs have decreased. Efficiency has increased and cost of construction has decreased and technology choices have become better. The second important reason is that renewable energy gives us the opportunity to fix energy costs for the medium to long term.

When we look at oil, coal or gas fired power, the fuel is a variable and remains a variable for a 20 to 25 year period. The price of fossil fuels is very volatile. The only thing you know for sure when you contract at a certain price today is that next year the price will be different. The only certainty is that there will be a change. It could go up or down. Often it is up. Sometimes it does come down for a few years. With solar energy there is no fuel cost. Everything can be contracted upfront. These are the reasons we see solar energy becoming more popular, faster.

About coal, you’re right, coal prices are down. But who knows when they will go up again? In energy, we are making long term choices, for 25 to 40 years. You don’t build a coal powered power plant and scrap it 5 years later. It is way too expensive and it has a technical life of 40 years. You’re locked in. You cannot make power plant commitments based on the price of coal today. I think what we are seeing is that governments and big utilities are recognizing the value of the diversity of fuel. They are looking for a mix, not putting all their eggs in one basket. It’s particularly important with the price volatility of fossil fuels. It’s better to have a hedge, taking advantage of lower prices when it’s available but also have security through diversity.

This is why countries like the UAE are looking to implement a coal powered power plant. Egypt is also exploring coal power plants. This doesn’t mean they will now only produce power from coal. I think they are making it clear that it is part of a mix, a small amount in the total portfolio. We will see more of this as we go forward. Except perhaps in places like Africa, where they don’t have too much of a choice. They are using their own natural resources. They used coal because they have it rather than substituting it with an imported fuel like gas or oil.

Let’s focus on Saudi Arabia, especially about renewable energy projects. What progress is Saudi Arabia making and what is the outlook?

About 4 years ago, the Saudi government under King Abdullah had made a decision to broaden the fuel mix. A new agency called K A CARE (King Abdullah City for Atomic and Renewable Energy) was created and assigned the specific responsibility of studying the possibility of introducing renewables and nuclear power into the fuel mix, formulating policies and coming up with a procurement plan. In my opinion, K A CARE did a fantastic job. It came up with a very firm proposal. However, because there are many parties involved in the energy sector, things got bogged down in discussions and analysis.

Understandably, these being fundamental policy decisions, it will take some time. During the past 4 years, the prices of renewable energy stayed fairly high. Then at the tail end of 2014, prices started coming down to such an extent that it is now a compelling value proposition, particularly photovoltaic and wind and even CSP. When the analysis began, about 3 years ago, it was 35 cents per kilowatt hour for CSP. This is fully dispatchable power, the heat is collected and stored, but it is usable day or night. It’s a wonderful alternative but it was very expensive. In just the last 18 months, that figure has come down to just about 15 and a half cents and is coming down further, fairly quickly.

Now, in 2015, many things are coinciding to change things. K A CARE’s policy formulation, more and more people being convinced of the case for adding renewables to the mix, and ARAMCO taking the lead in arguing to reduce the dependence on fossil fuels, particularly as we use fossil fuels at a subsidized rate, are all reasons for the changes. The new government is also taking the initiative forward. We fully expect to see deployment start in 2015. We will see a reasonably meaningful renewables program which will become the foundation on which we can build. As we deploy, and as the tariffs become even more competitive, the rate of deployment will accelerate.

In the medium to long term I anticipate the mix will be about 40% renewables, about 35 to 40% gas and less than 20% oil, which will subsequently fade away completely.

Nuclear is another option but a lot more studies will have to be done in due course.

There has been a change in leadership in Saudi Arabia, with a new king taking over. There’s also the challenge of the drop in oil prices and the competition of the shale gas and Chinese petrochemical expansion. It look like a storm heading towards Saudi Arabia. What is your opinion on these issues?

I am very optimistic in my outlook. I consider it a very good thing. Here’s why. I think the current drop in oil prices forces us to have a good cleanout and become more efficient. We will have to rethink our priorities and socioeconomic development policies. I think the fact that we have a new leadership is going to be helpful. I’m a great believer in change being always good. And I’m seeing that the change is very positive.

The price drop of oil makes us realize that we are a country that depends on a very volatile income base. Oil is the bulk of our income. We need to think about that and formulate policies around that.

What should be our first policy? Irrespective of how much money we have in reserve, we must first focus on conserving our cash. We must start diversifying beyond oil and gas. The country has many more natural resources which have not been tapped so far. We have human resources. The population is huge and it is young. That is a very valuable natural resource. It’s also got a lot of mineral resources. Sand and the sun are resources too.

Renewable energy can become an important anchor as we develop it for ourselves, we can also create an industry, we can create a knowledge platform and we can innovate. We can become a leader in that sector. In the future, we can even export that energy. It might not need ships and pipelines as with oil and gas, it can be wires. We can easily take this energy all the way to Europe and elsewhere.

The second area of focus for us would be to broaden the economy. Thirdly, as we diversify and grow the economy, we use the human capital to grow small and medium enterprises and absorb more people into the economy. I’m encouraged to see the new administration trying to get the private sector more plugged into the economy. This will allow the state to move away from economic activity into more of a regulatory, supervisory and governance role. I think the low oil prices and the new government in combination are a fantastic opportunity for Saudi Arabia. Saudi Arabia is handling it well and moving forward.

How will they cut entitlements, which will be a necessity if oil prices stay low?

I think it would be a big problem it was a 2 year timeframe. Ten years is a reasonable timeframe to develop other sectors. I already see the mining sector growing and that pace will accelerate. It will pick up some of the slack and start to generate some wealth. We are also beginning to see some serious industrialization activity. General Electric making gas turbines in Saudi Arabia. Siemens is no longer just assembling but making many of the components for gas turbines in the country.

Toyobo is now making membranes in Saudi Arabia. Some of the things that have been going on here are not so smart. Saudi Arabia consumes about 40% of the installed desalination capacity in the world. One of the biggest consumables in desalination are the membranes used in reverse osmosis. From the beginning of desalination up to about 2 years ago, the petrochemicals that go into making membranes, went from SABIC in Saudi Arabia to Japan, in raw form. It was turned into fibers in Japan and wound into a mesh. This would then be shipped back to Saudi Arabia at about a 150 time markup. They were phenomenally expensive membranes. Just 2 years, they started making membranes in Saudi Arabia.

That analysis is substantially correct, perhaps off by a few years. It will happen if we carry on as we were doing before, if the government continues to subsidize, give stipends and pour more money into the economy. Things have started changing. Within a week and a half of King Salman taking over things began to change. Normally Saudis don’t speak much at international gatherings. The Governor of the Central Bank, Fahd Mubarak, spoke up at the conference of central bank governors in India. Now all the ministers are speaking up. They are all mentioning the 4 priorities that Saudi Arabia is focusing on – conserving cash, diversifying the economy beyond oil and gas, job creation and privatization.

They are already starting to do it. It’s not that services will be cut but that the private sector will be delivering more of the services. They will continue to subsidize it for a while. The other thing they will do is move from capital expenditure to recurrent expenditure. That analysis would be right if we carried on with the old system of injecting capital expenditure. Saudi electric is a case in point. It was continually injected with capital, up to SAR 40 billion at a time. Going forward, that will stop. If the private sector takes over, the capital might still come in, but it will be spent over a longer period of time. The expenditure will be recurrent and the time will be used to wean away from subsidies. This will make the economy stronger and able to cope in an unsubsidized environment. Subsidize the poor and the disadvantaged. Unfortunately, the reality of subsidies is that they benefit the rich and the privileged.