Oil Market Outlook 2012

China is expected to be the main driver of oil demand growth with an expected increase of 0.42mn bpd in 2012.

Oil Market Outlook-2012

European debt crisis still lurking in the background

2012 will likely see Europe suffer from the hangover of the 2011 sovereign debt crisis. The 1H12 is crucial as major repayments come up. What happens in Italy is particularly important as it is the third largest economy in the region and accounts for around a third of the total debt repayments due in 1Q11. The crisis in the Euro-zone is likely to have an impact on oil prices as was witnessed in 2011 through its effect on the EUR/USD exchange rate. In addition, austerity measures undertaken by the regional economies to bring fiscal deficits to manageable levels will continue to have an adverse impact on oil demand growth in the region in the medium-term due to a slowdown in economic growth. IMF

World oil demand continued to recover, though at a slower pace. World oil demand increased by 0.9mnbd in 2011 after a strong increase of 1.6mnbd in 2010. European sovereign debt crisis, Arab Spring and Earthquake in Japan were the major factors which kept a lid on world oil demand growth.

now expects Euro-Area GDP to decline by 0.5% in 2012.

Increase in geo-political risk keeps oil prices high

Oil prices ended 2011 close to USD100.0 per barrel mark as political upheaval in the Arab world outweighed concerns over health of the global economy. The average price for 2011 increased by 19.6% to USD94.9 per barrel. World oil demand grew by 1.04%YoY in 2011 driven by demand in the emerging countries, particularly China. Threat of supply disruptions remained a major theme throughout 2011, particularly with the start of civil war in Libya which saw WTI prices spike above USD110 per barrel mark in 2Q11. The other dominant event has been the ongoing European debt crisis which threatens to throw a spanner in the global economic recovery. The IMF has already downgraded its estimate for world economic growth for 2012 in view of the prevailing risks

China to remain the main growth driver

China is expected to be the main driver of oil demand growth with an expected increase of 0.42mn bpd in 2012. The Chinese Central Bank increased the banks reserve requirement ratio six times and the interest rates three times in 2011 to curb inflation. However, in a surprising move the Central Bank cut the reserve requirement ratio in December indicating that the policy makers have turned their focus back on growth in view of the expected slowdown in Euro-zone and other advanced economies. China is likely to remain the main driver of crude oil demand growth for the foreseeable future despite the expected decline in GDP growth rate to 8.2% in 2012.

Modest growth seen for US in 2012

The US economy seems to be trudging along despite the headwinds from the Euro-zone crisis and overhang of high debt and deficit. US unemployment declined to 8.5% in December after staying above 9.0% for a large part of 2011. The IMF now estimates US economy to grow by 1.8% in 2012. Recovery in the US economy, the world’s largest oil consumer, will play a large role in determining the direction of oil prices. The US Federal Reserve has said that its benchmark interest rates will stay low at least till late 2014 to spur economic activity and bring down unemployment further.

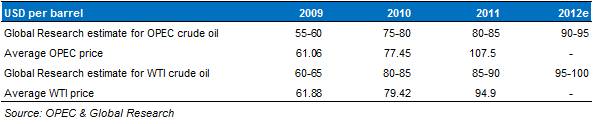

WTI crude oil prices expected to be around USD95-100 in 2012

Global Research expects average WTI crude oil price to be in the range of USD95-100 in 2012 which is also consistent with the Bloomberg Consensus crude oil price of around USD98.7 per barrel and close to 2011 average price of USD94.9 per barrel. Our 2011 estimate (given in Oil Market Outlook 2011) for WTI was close to the actual price. However, our estimate for OPEC crude oil deviated by 26-34% as impact of Arab spring was felt heavily in the regional crude oil prices.

Volatility to persist; Major risks still exist

The volatility in 2011 is likely to extend into 2012 as the European debt crisis remains unresolved, Arab Spring continues and unemployment remains high in the US. Meanwhile, new sanctions on Iran and subsequent military drills by the Iranian Navy in the Strait of Hormuz has increased the risk of stand-off between the US and Iran which could severely disrupt oil supplies. The transition of power in North Korea has also increased the geo-political risk with lack of clarity over the direction the isolated country will take.

OPEC Production and Spare Capacity

OPEC makes up for loss of production in Libya

Political turmoil in the Middle East had a direct impact on OPEC oil production as Libya descended into civil war. Production in Libya fell to 47tbpd in 3Q11 compared to an average production of 1.55mnbpd barrels in 2010. However, the shortfall was filled in quickly with Saudi Arabia in particular raising its production to 9.6mnbpd in 3Q11 from 9.1mnbpd in 2Q11. However, the production in Libya is on the road to recovery as the Transitional National government has taken over. Crude oil production in Libya has increased to 0.77mnbps in December 2011.

Spare capacity sufficient to make up for decrease in Iranian exports

Saudi Arabia still commands the largest spare capacity of around 2.71mnbpd despite the increase in production in 2011. This holds particular significance at a time when Iran is coming under further pressure because of its nuclear program. European Union plans to halt oil imports from Iran as part of the sanctions. Gulf nations are ready to make up for loss of exports from Iran according to a Saudi official as reported in the media. As can be seen in the table below, the Gulf countries, and in particular Saudi Arabia has the capacity to fill the production gap.

World Oil Demand

World oil demand continued to recover, though at a slower pace. World oil demand increased by 0.9mnbd in 2011 after a strong increase of 1.6mnbd in 2010. European sovereign debt crisis, Arab Spring and Earthquake in Japan were the major factors which kept a lid on world oil demand growth. The recovery in 2011 and 2010 came after a steep decline in 2009 by 1.4mn bpd and a slight decline in 2008. The decline in 2008 was the first decline in oil demand since 1983 reflecting the impact of the global financial crisis and the ensuing recession. The global financial system is going through turbulence with debt crisis in Europe taking the centre stage. The impact of the crisis manifested itself in Western Europe Oil demand which declined by 0.16mnbd reflecting the impact of the austerity measures.

China to continue to drive oil demand growth in 2012

World oil demand is expected to increase by 1.21% to 88.9mnbpd. Bulk of the world oil demand growth is expected to come from China, Latin America and the Middle East region. Increase in China’s oil demand is expected to contribute around 40.0% to the total oil demand growth in 2012. Fears of hard landing in China have faded with inflation in China coming down to 4.2% in November and a cut in reserve requirement for banks, indicating a change in focus by policy makers.