Insurance in Ivory Coast: Bernard Abouo Presents La Loyale

When we talk about insurance in Africa, Ivory Coast is the country that has seen a lot of development over these last decades, above all in life insurance. Whilst notable advancements have been recorded, we must recognise that there still remains a lot to develop here.

Interview with Bernard Abouo, CEO of La Loyale Assurances and Board Chairman of La Loyale Vie

What is your overview of the sector in general? Where do you stand in terms of competition and foreign investors? Are you in a situation where there are plenty of players?

The insurance sector is doing well. It is constantly evolving here on the continent. Ivory Coast has always been the market leader in terms of turnover in the CIMA region as well as in Western and Central Africa. For a long time, this market has been dominated by subsidiaries of European insurance companies, mostly French companies.

Thus in terms of progress, l’Union Africaine, a subsidiary of UAP (Union des Assurances de Paris), has been the market leader. This company consequently became AXA Cote d’Ivoire after UAP was bought out by AXA. Another company that was present was AGF (Assurances Générales de France) via their subsidiary AGCI (Assurances Générales de Cote d´Ivoire).

Little by little the large groups have left. Some subsidiaries have stayed or have been bought out by African companies, whilst others have merged. Colina, after the recovery of Groupama, has become one of the largest companies in terms of structure. Recently they have been bought out by Saham.

As a result, the African companies came about. Initially they were created by the State as national insurance companies. Only in Ivory Coast were there private companies at the same time as national companies. Gradually the other countries have followed in this way.

When we talk about insurance in Africa, Ivory Coast is the country that has seen a lot of development over these last decades, above all in life insurance. Whilst notable advancements have been recorded, we must recognise that there still remains a lot to develop here.

Which are the main areas that need development? What are the main shortcomings?

The main shortcomings are principally in terms of education in insurance culture. This will really create an impetus for the sector; once our population understands the importance of insurance and incorporates it into their consumer habits.

In France, in order to get a loan we are legally obliged to have insurance, otherwise we cannot get a loan.

Here it is the same; in order to get a bank loan you are required to have a life insurance policy in order to guarantee the loan repayment in case the borrower dies. In fact, we can note that our best clients are those that have already had to claim on their insurance and have benefited from the remunerations given by the insurers.

Nevertheless a recent survey undertaken by the Insurance Board has shown that a large proportion of the automobiles in circulation in our country are not insured, in complete disregard to the risks incurred. Whilst in Europe one would never think to have a car that is not insured, in our market, this is not the case yet. Thus it is insurance education that we have to instil.

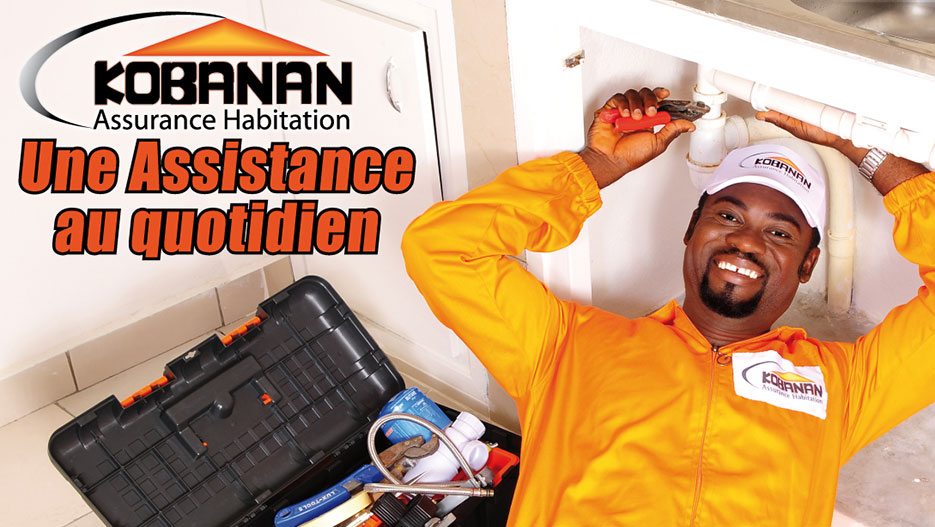

This will occur through the adaptation of insurance products to the cultural and social realities of the population and through assistance to policy holders in order to make the products more useful to them in their daily lives. In actual fact, people notice the assistance given to them more than the actual product itself. Thus here at La Loyale Insurance, we have with this objective in mind, placed a home insurance product on the market called Kobanan, which means “no problem” in a language from the north of our country. Kobanan is designed with support, to insure the home, its contents and its residents. The integrated support allows the policy holder to deal with domestic repairs with just a simple telephone call, which we follow up by sending out a professional.

In my opinion, we have to explain to the population that insurance is a question of solidarity; it is the mutual management and repartition of risk.

In conclusion, we can say that we are seeing good development of the insurance sector in Africa in general. As a matter of fact, South Africa, which used to represent more than 80% of the volume of insurance policies, has seen its share reduced to 75% due to the increase in volume of insurance policies throughout the Maghreb region and the CIMA region where we are seeing good progress.

Thus, it is something that is not rooted in African habits. However in South Africa they have the European reasoning?

Yes. The Europeans that developed South Africa had the time to instil this kind of insurance culture in the population before leaving. However, this was not the case for all African countries. It is up to us Africans, governors and insurers to succeed in educating our population in order to develop our nations now.

Tell us about the two divisions of La Loyale. What are the competitive advantages of the company over the other players of the sector?

La Loyale group is composed of two private limited companies: La Loyale Vie specialised in life insurance and La Loyale Assurances specialised in non-life insurance. They were created respectively in 2003 and 2004, each with a share capital of 1.5 billion CFA francs in 2009.

Since its creation, the group has captivated the public’s attention through its innovation with products that are adapted to the needs of the population. Thus, the group has been in 6th place in the Ivorian insurance market for several years.

Our products are designed to be solutions or responses to the problems that economic players and the population encounter with regards to insurance and social security.

This is certainly the case with the product called IFC, Indemnity for Career Termination, which allows companies to have sufficient funds available to deal with the charges incurred when an employee leaves. Normally the company establishes the funds to this effect. With IFC, the employer transfers these charges to the insurer and benefits from the fiscal advantages on the liabilities, established with the insurer.

Yako is a funeral insurance product that we have designed to guarantee the policy holder a dignified burial thanks to the benefits in kind that we offer in the case of bereavement: collection, care and preservation of the body, removal of the body, allocation of a coffin and transportation to the burial site. The family also receives a cash sum. Many families get into debt to pay for the burial of a loved one because funeral services are of great social importance. This product gives a family both support and assistance in this respect. The strong demand for this product has pushed us to create a wide range within this segment to respond to the various needs and budgets. As this product is so practical many of our clients are in fact living abroad and those that have already benefited from the product go on to recommend it.

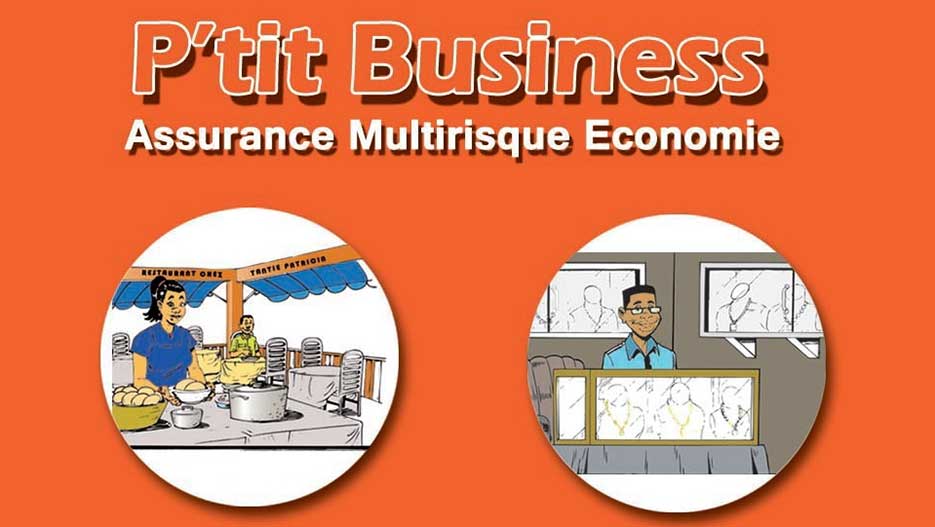

Our product P’tit Business is dedicated to economic players from the tertiary sector where investments are not that high: hair salons, sewing workshops, scripters, restaurants and so on. This product allows these businesses to benefit from an insurance cover designed for their scale but covering the same risks that any economic player faces and which could lead to the definitive cessation of activities: fire, theft, water damages, etc. And we have also added an individual accidents cover for the employer and/or their employees to cover them in case of any accidents.

All of our products are therefore designed to respond to the economic and social problems faced by the African population in general in their professional and private lives.

La Loyale is part of Globus Network. What does this mean for you and your clients?

Multinationals such as Bouygues and Bolloré in France use Globus Network. This network has been set up to help the large groups and to facilitate their brokers in the management of their subsidiaries’ insurance programs and the coverage of their investments in the African continent. The Globus Network is therefore a unique intermediary for a globalised offer, no matter what language is used in the country or where the client´s activities take place. Globus Network has a representative in each country. It is very advantageous for the clients who can receive within 48 hours, without leaving their office or home, a global offer for their insurance cover throughout the continent.

In very little time, all of the players have understood the importance of this network. Thus we have gone from being 8 member countries to 40 today, covering all languages: English, Portuguese, French and Arabic.

Our clients consider us to be partners. We organise seminars where we invite specialists to train our members in risk insurance. Responsiveness is required in this network. The Globus Network has for the last four years had a reinsurance captive company, Globus Ré, which plays the role of a centre for purchasing reinsurance, on behalf of its members, from leading worldwide reinsurers such as Munich Re, Swiss Re, Score, etc.

And the cases are filed within 48 hours?

Yes, that is the responsiveness of Globus. In 48 hours at the most, an insurance offer is forwarded to the client or international broker. We have thus succeeded in retaining our international clients.

Can you tell us a bit about your company policy and your desire to conquer Africa?

When we talk about insurance in Africa, Ivory Coast is the country that has seen a lot of development over these last decades, above all in life insurance. Whilst notable advancements have been recorded, we must recognise that there still remains a lot to develop here.

La Loyale’s goal is to conquer Africa after having consolidated our bases in Ivory Coast. We are working hard to achieve this goal and to find the funds and partners to apply our policy. Certain countries have potential, but we are sometimes surprised to find that their turnover represents that of just one company in Ivory Coast. Our policy could help the development of insurance. In Ivory Coast, we are developing and our turnover is increasing. We hope to set up all over Africa wherever the opportunities present themselves.

Regarding this foreign expansion, do you need local partners?

You always need local partners. We believe that the manager ought to be a local partner.

You mentioned a good financial rating that created some buzz in the media. Can you tell us a bit more about this?

In terms of Globus Network, when we began to work with the Anglophone countries, we understood that they preferred rated companies. Thus, we have sought out a specialised rating company called Bloomfield Investment, to proceed with the financial rating of our companies. The publication of this rating in various international journals has earned us the confidence of new foreign clients who have come to invest in Ivory Coast. We understood that rating is very important and that it equates to transparent management. It is a very good thing and it has brought us a lot, not only us, but to all those in the Globus Network that participated in the rating.

If you look forward to the medium term, what do you imagine the situation to be like for La Loyale?

Our goal is to be a profitable company, but the most important thing is the education that we have to give regarding insurance. In the next 3 years, we foresee to be in the top 5 companies in the Ivorian market and to be present in 4 or 5 African countries.